Club GTI Club GTI

Club GTI Club GTI

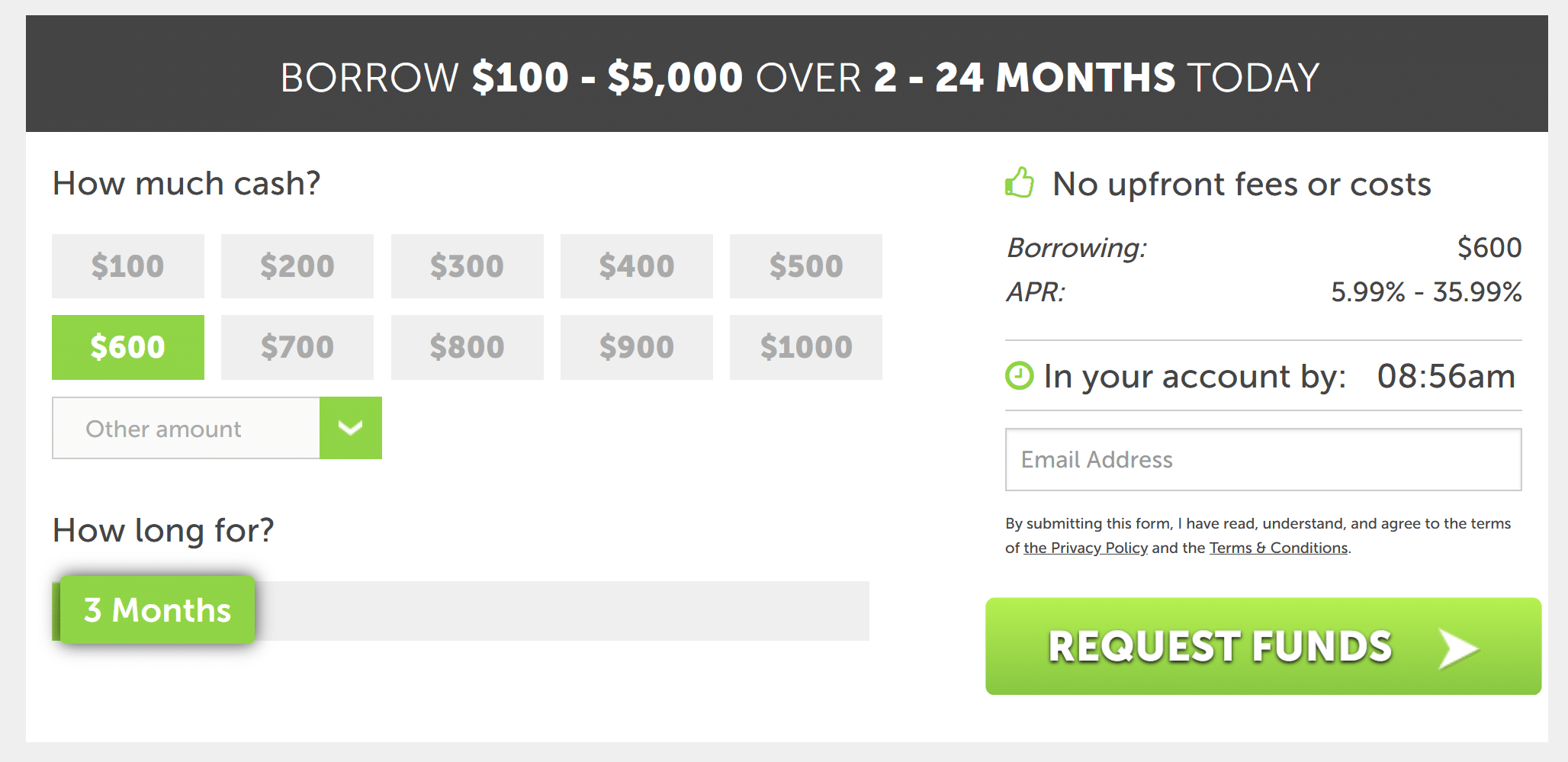

Payday loans are short-term loans needed to compensate for frivolous immediate losses. The lender allows the needy person a loan and holds the person's check (usually until the day the customer's salary is due) before giving the check to the intermediary user's bank for reimbursement. The annual interest rate on these loans is consistently fabulously high, ie. 410% or more. Payday loans are an adventurous kind for a person taking out a loan. In all likelihood, it makes sense for you to be wary of taking payday loans. It is unfortunate that some payday lending activities have used fiction and some illegal activities to take advantage of financially needy consumers looking for these loans.

What do I need to bring with me before I apply?

To apply for a loan you will need:

- Any document issued by the state authorities and for certifying your person with a photo

- You must show your social security number

- A functioning and serviceable phone number

- Certification of the most recent income notices

- You must have at least 30 calendar days of your checking deposit active

How do payday loans work?

The Bureau of Economic Security states that 77% of payday loans same day are not repaid within the time period specified in the contract. The situation is worse with web borrowers. This leads to the fact that the interest cost decisively increases and the payment you owe increases, making it ultimately unrealistic to repay it. In the event the payday loan and proper interest is not paid at the specified time, the payday lender is able to deposit the user's check. There are variations that the consumer has too little money in the deposit to close the cash advance. Depending on the rules of the loan, you will become given to a contribution institution or a debt collector, and these agencies have every chance of putting you on the debt reporting society's radar.

Cash advances have become highly sought-after in the U.S. According to the Consumer Financial Protection Bureau (CFPB), in 2015, 36 states had more payday lending locations than McDonald's locations in any of the 50 states. Payday loans operate at payday lending locations or at locations that sell other financial services, including check cashing, secured loans, rent-to-own, and deposit, according to state licensing requirements.

Payday loans function in a different way than individual and other consumer loans. A consumer can have a maximum of two payday loans at a time, they cannot be with the same payday lender and every loan is limited to $500-$999, not including taxes. Different states have different laws regarding payday loans, which limit the amount of money you can borrow, or the amount of money a lender can charge in interest and fees.

Credit scores can change for the worse if payday loans are taken out

A payday loan online same day does not require a determination of your ability to pay back the loan or proof of your ability to liquidate the loan. Payday lenders routinely don't perform a credit examination on applicants, so submitting a request won't be described as a tough request in your financial review, and they won't bring credit reports to the agency's attention when you acquire them. They additionally usually don't notify any information about your payday loan history to nationwide financial companies. But according to Experian, these loans additionally can't help you establish your credit when they are not reported to the credit transaction bureaus as soon as you pay them on commission.

The truth is, things change as soon as your credit profile is made delinquent. On the off chance that you don't repay your loan and your lender sends or sells your payday loan obligation to a problem loan collection company, the debt collector is probably in a position to put in a notification of this debt to one of the big state banking companies. In such a situation, it is still in a position to harm your credit history. On the off chance that it does, it will remain on your financial file for seven years and critically affect your debt history. Financial points are summed up by several all sorts of credit offices based on the data the office concentrates on people. Not paying off your payments on time will cause your points to drop, which has the potential to significantly affect your upcoming loans.

How MCA is coordinated in the United States

In 2017, the Consumer Money Safety Apparatus made several changes to laws to support protect people who take out loans, including forcing payday lenders, which the apparatus calls "small box lenders," to fix whether a borrower can afford to make a loan with an interest rate of 390%. The laws encompassed an inherent underwriting rule, a proper for lenders to rate a borrower's ability to liquidate a loan and still compensate for everyday living expenses before a loan is made. But the Trump administration rejected the judgment that consumers have a need for security, and the CPFB abolished the underwriting provision in 2020.

Payday loans at triple-digit rates and with comprehensive closing in the second pay period are considered legal in states where lawmakers have either repealed the regulation of small loans or abolished payday loans from traditional small loans or usury laws and/or enacted legislation authorizing loans based on a check from the person making the loan or an electronic payment from a bank account.

It is imperative that a principle be adopted to guarantee subsidiary protection for people who take credit. In addition, other and legal tactics of trade credit must be developed. Parliament and the states, in turn, are working to expand security, among other things to implement a 35% interest rate quota for all states. The few states that give payday lending work the maximum loan amounts, as usual from $350 to $950.

Payday loans are not permitted for active duty service members and their dependents. Laws also determine the time period of the loan - in many cases it is as little as 10 days - but in many states there is no limit on the duration of the loan. Going forward, we may feel more and more regulation of this type of source of income.

Is it allowed to borrow a payday loan without a debit account at a financial institution?

Yes. Having a financial deposit is not always necessary in order to borrow money, but lenders who do not require it tend to charge high interest rates. Yes, and you should still be able to prove that you have the necessary income to liquidate the loan. Payday lenders will be able to ask for a financial deposit, but in some cases a paid bank deposit may be sufficient to acquire the basis for the loan. Not all lenders will accept this kind of loan project, so it will be advisable for you to do some research to discover the right lender that does.

If only the lender approves your debt application and you don't have a bank account to plan for repayment, you will probably need to build a strategy to make the payment yourself by money order, check, cash. It is best to liquidate a short-term debt before its repayment deadline, as a cash loan has the ability to conclude costly consequences for not meeting the repayment time.

Getting a payday loan can be more difficult, and even if a lender goes to work with you, they may need a lot more data and documentation before they feel comfortable lending you money. The lender will in all likelihood try to verify that you don't have an unopened case of bankruptcy, passing accounts or active tax debts to your state. Without a bank deposit, you are, in most cases, cut down on short-term loans, including quick payday loans with a bad debt history or secured home loans.

What Americans need to focus on before borrowing a payday loan

Surveys note that 12 million U.S. customers get payday loans every year, despite the abundant evidence that they lead most borrowers into significantly substantial debt. However, people who have gotten payday loans for the most part do not indulge in speculation that they can borrow cash elsewhere, there are options that they should discuss.

What can a cash advance be?

The employer's cash advance is formally considered loan resources, but it does not have to be repaid. A wage advance is an economic contingency between an employer and a subordinate. You take as a favor from your paycheck, the money is directly given to you by your employer before you are routinely paid. Every paycheck advance is supposed to be approved in effect. Every written request for a payday advance forms a paper sign, and also can very well be beneficial in case any problems are created with the employee (payroll deviation, reduction, etc.). By creating a project of providing money at work, administrations have all the chances to provide an opportunity with a small possibility of danger to workers who have a need for certain funds. This could very well be a superb technique to dodge the classic debt fees, online add-ons and the litigation of writing an application.

Online counseling services for existing debts

Government credit counseling agencies, such as InCharge Debt Solutions, offer free suggestions on how to determine a clear monthly settlement and avoid debt. In order to spot a debt consulting agency, go on the web, talk to a credit union, housing authority manager then or hiring service for recommendations.

PAL or PAL II is a much better alternative for payday loans

Alternative payday loans, or PALs, enable members of formed federal loan unions to lend moderate amounts of financial resources at a lower cost than classic payday loans, and cancel the loan over a much longer stage. You can practice living money from PALs, to dodge a payday loan or to pay off an existing one. PALs are managed by the national administration of debt organizations, which formed the initiative in 2011. The highest interest rate for PALs is 31 percent, which is almost one-fifteenth of the price of a mediocre payday loan. In 2017, NCUA added a second PAL option, notorious as PALs II, which has similar requirements. Moreover, credit alliances are prohibited from extending PALs, indicating that borrowers are less likely to fall into a predatory debt cycle. Loan borrowers own the right to draw only 1 type of PAL at a time.